The Thrift Savings Plan (TSP) is one of the most important financial tools available to federal employees and members of the uniformed services in the United States. It provides an opportunity for individuals to save and invest for retirement while enjoying significant tax advantages. Understanding the intricacies of TSP and staying updated on the latest discussions and changes is crucial for maximizing your retirement savings.

In this article, we will delve into the world of TSP Plan Talk, exploring its features, benefits, strategies, and the latest trends. Whether you're a seasoned investor or just starting your retirement planning journey, this guide will provide you with actionable insights and expert advice to help you make informed decisions about your TSP account.

From understanding the basics of TSP to exploring advanced strategies, we will cover everything you need to know about TSP Plan Talk. Let's dive in and explore how you can optimize your retirement savings through the Thrift Savings Plan.

Read also:Movies4u Vip Exclusive Streaming

Table of Contents

- What is the Thrift Savings Plan (TSP)?

- Benefits of the Thrift Savings Plan

- Overview of TSP Plan Talk

- Investment Options in TSP

- Contribution Limits and Catch-Up Contributions

- Tax Advantages of TSP

- Strategies for Maximizing TSP Benefits

- Latest Discussions in TSP Plan Talk

- Common Mistakes to Avoid in TSP Planning

- Conclusion

What is the Thrift Savings Plan (TSP)?

The Thrift Savings Plan (TSP) is a tax-advantaged retirement savings plan offered to federal employees and members of the uniformed services in the United States. It functions similarly to a 401(k) plan in the private sector but is specifically designed for government employees. TSP allows participants to contribute a portion of their salary on a pre-tax or Roth basis, offering various investment options to grow their retirement savings.

Established by the Federal Employees' Retirement System Act of 1986, TSP has become an essential component of retirement planning for federal workers. With its low fees and robust investment options, TSP is considered one of the best retirement savings plans available today.

Key Features of TSP

- Low administrative fees compared to other retirement plans.

- Access to professional fund management.

- Government matching contributions for certain employees.

- Multiple investment options, including lifecycle funds (L Funds) and individual funds.

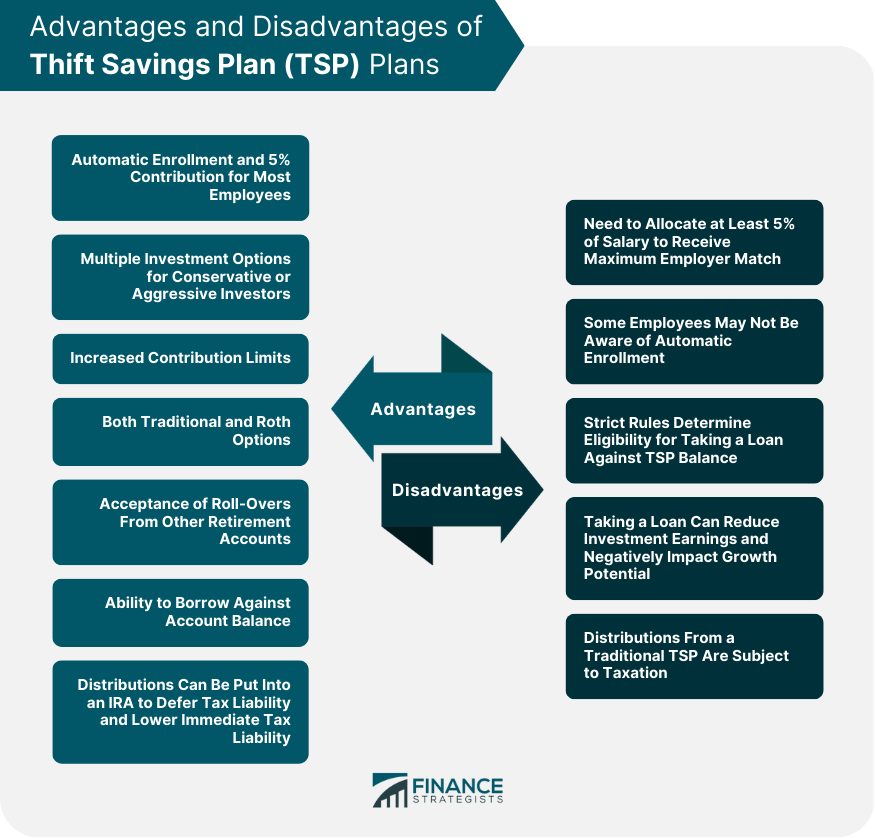

Benefits of the Thrift Savings Plan

The Thrift Savings Plan offers numerous advantages that make it an attractive option for retirement savings. Below are some of the key benefits:

1. Tax Advantages

TSP offers both traditional and Roth accounts, allowing participants to choose between tax-deferred growth or tax-free withdrawals in retirement. This flexibility enables individuals to tailor their savings strategy to their financial situation.

2. Low Costs

TSP is known for its exceptionally low expense ratios, making it one of the most cost-effective retirement plans available. This means more of your money stays invested, working for you over time.

3. Government Matching Contributions

Federal employees under the Federal Employees Retirement System (FERS) receive matching contributions from their employer, effectively doubling their retirement savings potential. This employer match is a valuable benefit that should not be overlooked.

Read also:Free Movies Tv Shows Movirulz Latest Releases

Overview of TSP Plan Talk

TSP Plan Talk refers to the ongoing discussions, updates, and insights shared by financial experts, government agencies, and participants regarding the Thrift Savings Plan. These conversations cover a wide range of topics, from changes in contribution limits to new investment options and strategies for maximizing TSP benefits.

Staying engaged with TSP Plan Talk is essential for anyone looking to optimize their retirement savings. By keeping up with the latest trends and updates, participants can make informed decisions about their investments and take full advantage of the plan's features.

Investment Options in TSP

One of the most appealing aspects of TSP is its diverse range of investment options. Participants can choose from a variety of funds, each with its own risk and return profile:

1. Lifecycle Funds (L Funds)

Lifecycle funds are designed to automatically adjust their asset allocation over time, becoming more conservative as the participant approaches retirement. These funds are ideal for those who prefer a hands-off approach to investing.

2. Individual Funds

- G Fund: Invests in government securities and is considered the safest option within TSP.

- F Fund: Invests in a mix of government and corporate bonds, offering moderate risk and return.

- C Fund: Tracks the performance of the S&P 500 index, providing exposure to large-cap U.S. stocks.

- S Fund: Invests in small- and mid-cap U.S. stocks, offering higher growth potential but with increased risk.

- I Fund: Invests in international stocks, providing diversification and exposure to global markets.

Contribution Limits and Catch-Up Contributions

The Internal Revenue Service (IRS) sets annual contribution limits for TSP accounts, which are subject to change each year. For 2023, the maximum contribution limit for TSP is $22,500 for employees under age 50. Those aged 50 and older can take advantage of catch-up contributions, allowing them to contribute an additional $7,500 to their TSP account.

It's important to note that these limits apply to both traditional and Roth TSP contributions combined. Participants should carefully plan their contributions to maximize their savings potential while staying within the IRS limits.

Tax Advantages of TSP

TSP offers several tax advantages that make it an attractive option for retirement savings:

1. Traditional TSP

Contributions to a traditional TSP account are made on a pre-tax basis, reducing taxable income in the year they are made. The contributions and earnings grow tax-deferred until withdrawal, at which point they are taxed as ordinary income.

2. Roth TSP

Roth TSP contributions are made with after-tax dollars, meaning they do not reduce current taxable income. However, qualified withdrawals from a Roth TSP account are tax-free, providing a significant advantage in retirement when income may be higher.

Strategies for Maximizing TSP Benefits

To get the most out of your TSP account, consider implementing the following strategies:

1. Take Advantage of Employer Matching

For FERS employees, the government matches a portion of your contributions up to 5% of your salary. This is essentially free money, so it's important to contribute at least enough to receive the full match.

2. Diversify Your Investments

Spreading your contributions across multiple funds can help mitigate risk and optimize returns. Consider using L Funds for a balanced approach or creating a custom allocation with individual funds.

3. Regularly Review and Adjust Your Portfolio

Market conditions and personal circumstances can change over time, so it's important to regularly review your TSP portfolio and make adjustments as needed. Rebalancing your investments ensures your portfolio remains aligned with your retirement goals.

Latest Discussions in TSP Plan Talk

TSP Plan Talk is constantly evolving, with new developments and discussions emerging regularly. Some of the latest topics include:

1. Changes in Contribution Limits

The IRS periodically adjusts contribution limits to account for inflation. Staying informed about these changes can help participants plan their contributions effectively.

2. New Investment Options

TSP occasionally introduces new investment options to provide participants with more flexibility and diversification. For example, the addition of the I Fund in 2001 expanded access to international markets.

3. Impact of Market Volatility

Market fluctuations can have a significant impact on TSP investments, especially for those nearing retirement. Experts often discuss strategies for managing risk during periods of market volatility.

Common Mistakes to Avoid in TSP Planning

While TSP is a powerful retirement savings tool, there are common mistakes that participants should avoid:

1. Not Taking Full Advantage of Employer Matching

Failing to contribute enough to receive the full employer match is one of the biggest mistakes TSP participants can make. This is essentially leaving free money on the table.

2. Overlooking Roth Contributions

Roth TSP contributions offer significant tax advantages in retirement, but many participants overlook this option. Evaluating your current and future tax situation can help determine whether Roth contributions are right for you.

3. Neglecting Regular Portfolio Reviews

Failing to regularly review and adjust your TSP portfolio can lead to missed opportunities and increased risk. Staying proactive in managing your investments is key to achieving your retirement goals.

Conclusion

The Thrift Savings Plan (TSP) is a vital component of retirement planning for federal employees and members of the uniformed services. By staying engaged with TSP Plan Talk and implementing sound investment strategies, participants can maximize their retirement savings potential.

We encourage you to take action by reviewing your TSP contributions, diversifying your investments, and staying informed about the latest developments in TSP Plan Talk. Don't hesitate to leave a comment or share this article with others who may benefit from its insights. Together, we can build a secure financial future for ourselves and our families.